Have you ever dreamt of owning your own home, embarking on a dream vacation, or finally upgrading your outdated car? These desires, while exhilarating, often come with a hefty price tag. But achieving these goals doesn’t have to feel like an impossible climb. The answer lies in strategizing and implementing a robust savings plan. This article serves as your comprehensive guide to mastering the art of saving for those large purchases, equipping you with the knowledge and tools to turn your aspirations into reality.

Image: www.chegg.com

Saving for a substantial purchase isn’t just about stashing away money; it’s about crafting a financial roadmap that leads you steadily towards your goal. This roadmap factors in your income, expenses, spending habits, and most importantly, your financial aspirations. Whether you’re aiming for a down payment on a house, saving for a wedding, or planning a world-tour, understanding the principles of effective saving is crucial.

Setting Your Sights: Defining Your Goals

1. Dream Big, Plan Smart

The journey towards your financial goals starts with a clear vision. What exactly are you saving for? Is it a dream home in the suburbs, a lavish wedding celebration, a year-long backpacking adventure, or perhaps a brand-new car that’s been calling your name? Visualizing your ultimate goal serves as a powerful motivator, keeping you focused and pushing you towards your target.

2. Quantify Your Dreams

Once you have a clear image of your desired purchase, the next step is to assign a concrete number to it. For example, if you’re aiming for a house, determine the price range you’re comfortable with. This number will serve as your North Star, guiding your financial strategy and giving you a tangible target to strive for.

Image: www.chegg.com

3. Time is of the Essence

Now, let’s consider the time frame. How long do you have to save for this purchase? Is it a short-term goal (like a vacation next year) or a long-term goal (like retirement)? Establishing a realistic timeline helps you determine how much you need to save each month to reach your goal within the specified timeframe.

Building a Strong Foundation: Understanding Your Finances

1. Factoring in Your Income

Knowing your consistent income is essential for financial planning. Analyze your earnings, taking into account any bonuses, raises, or part-time work. This income stream forms the foundation of your savings plan, providing you with the resources to achieve your goals.

2. Identifying Expenses: The Art of Budgeting

To know where your money is going, you need to understand where it’s coming from. This means taking a deep dive into your expenses. Analyzing your spending patterns helps you identify areas where you can make adjustments and allocate more towards your savings.

3. Budgeting Tools: Your Financial Allies

There are various helpful tools available to make budgeting a breeze. Consider using free online budgeting apps, spreadsheets, or dedicated personal finance software. These tools can track your spending, categorize your expenses, and even create spending reports, empowering you with greater financial control.

Crafting Your Savings Blueprint: Strategic Approaches

1. Saving Methods: The Right Fit for You

There are several popular saving methods that can help you achieve your financial goals. Let’s explore some of the most effective techniques:

- The 50/30/20 Rule: This rule divides your income into three categories: 50% for needs (housing, utilities, groceries), 30% for wants (entertainment, dining out), and 20% for savings and debt repayment. This method promotes a balanced approach to spending and saving.

- The Snowball Method: This focuses on paying off small debts first to gain momentum and motivation. Once a debt is cleared, you roll that payment amount towards the next debt, creating a snowball effect that quickly reduces your financial obligations. This method works well for paying off multiple debts quickly.

2. Utilizing Your Savings: Smart Strategies

Once you’ve established a steady savings flow, it’s time to consider how to maximize the potential of your hard-earned money. Think about these approaches:

- High-Yield Savings Accounts: Choose a bank that offers competitive interest rates on savings accounts. This allows your money to grow even while it’s saved, amplifying your financial progress over time.

- Certificates of Deposit (CDs): Consider CDs for longer-term savings goals. CDs offer fixed interest rates for a set period, allowing you to lock in a steady return on your investment. This method is ideal for planning for a goal in the future, such as a down payment on a house.

- Investing: Explore investment options like stocks, bonds, or mutual funds if you’re comfortable with a higher level of risk. Investing can potentially yield higher returns than traditional savings accounts, but it comes with more volatility.

The Power of Discipline: Staying the Course

1. Staying Focused: The Importance of Consistency

Saving for a large purchase demands discipline and consistency. Stick to your budget even when temptations arise. The key is to prioritize your financial goals and make saving a habit. Just like brushing your teeth, make saving a regular part of your daily routine.

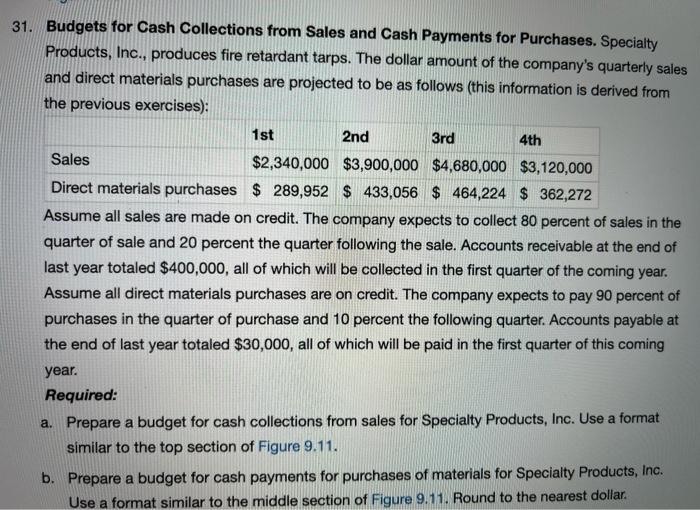

2. Facing Challenges: Overcoming Setbacks

Life throws curveballs. Unexpected expenses or job changes can disrupt your savings plan. If a setback occurs, don’t be discouraged. Reassess your budget, make adjustments as needed, and refocus on your goal. Remember, even a small amount saved each month can add up over time.

3. Seeking Help: Financial Guidance for Success

Don’t hesitate to seek professional advice if you’re unsure about how to navigate your financial journey. Financial advisors can create a personalized plan that aligns with your individual needs, goals, and risk tolerance. They can provide valuable insights and support, helping you make informed financial decisions.

Real-life Examples: Inspiring Stories of Savings Success

To illustrate the power of saving, let’s look at a couple of real-life success stories:

- The Down Payment Dream: Amelia, a young professional, set a goal to buy a condominium within the next five years. She created a detailed budget, tracked her expenses meticulously, and consistently contributed a portion of her income to a high-yield savings account. Through disciplined saving and smart financial management, she was able to achieve her goal ahead of schedule and enjoy the freedom of homeownership.

- The Adventure Fund: David, a travel enthusiast, had his sights set on a backpacking trip through Southeast Asia. He created a “travel fund” and dedicated a portion of his salary to it each month. He actively sought out ways to minimize expenses, such as cooking at home and using public transportation. By being mindful of his spending and saving consistently, he successfully accumulated enough funds for his dream adventure.

Saving For Large Purchases Answer Key

Conclusion: Your Path to Financial Freedom

Saving for large purchases is a journey that requires dedication, discipline, and a clear financial roadmap. By defining your goals, understanding your finances, and implementing effective saving strategies, you can turn your aspirations into a reality. Remember, every penny saved brings you closer to achieving your dreams. Embrace the power of consistent saving, and unlock the financial freedom to pursue your goals with confidence.